Open Banking: Banks per Countries - PART 2

In Part 1, we began our journey through the world of Open Banking, moving from the rule-bound streets of Brussels to the vibrant, entrepreneurial avenues of New York. Our next stop: Asia — from its bustling mega-tech cities to emerging digital hubs — where innovation thrives in mobile-first societies. Rapid digital innovation, expanding mobile-first populations, and forward-looking policies are driving Open Banking adoption faster than ever in this region.

While Europe’s regulatory-first approach and North America’s market-driven model set strong examples, innovation doesn’t follow a single beaten path.

Across Asia, Open Banking is evolving with bold determination, fueled by a shared drive for financial inclusion, mobile accessibility, and fintech empowerment. Countries like India, South Korea, and China are taking the lead by building systems that make financial services work better together. From India’s groundbreaking digital public infrastructure to South Korea’s advanced mobile banking platforms—local priorities are reshaping the future of global finance.

The East isn’t just following others — the continent is creating its own approaches that rethink old systems, revolutionizing Open Banking along the way.

What lessons can businesses learn from these diverse, fast-changing markets? At Contiant, we’re continuing our global tour to spotlight how Asia is advancing the Open Banking evolution — one API at a time.

Asia’s Open Banking Gold Rush: How Mobile-First Fintechs Are Transforming Finance

Asia is adopting Open Banking with great speed, transforming its financial landscape through the power of open APIs. This innovative model is reshaping how banks and fintechs collaborate, creating an ecosystem that ensures secure access to customer data to deliver smarter, faster, and more personalized services. Originally a concept born in the UK, Open Banking has now taken strong root across Asia, fueled by a growing API-driven economy and the region’s appetite for seamless digital experiences. According to a recent Finastra survey, financial institutions throughout Asia are already benefiting from this shift. They are responding to growing customer needs with new solutions that make everyday banking more and more convenient.

Open Banking is gaining strong momentum in both Hong Kong and Singapore, driving collaboration and efficiency in the financial sector — even during the challenges caused by the COVID-19 pandemic.

Here’s a closer look at these dynamic hubs:

- Hong Kong: An impressive 95% of banks have identified collaboration between them and fintech companies as a major reason for their success in the market. However, 43% of financial institutions see regulatory hurdles slowing down progress. The pandemic has only accelerated the push towards remote and digital banking, making Open Banking more vital than ever.

- Singapore: Nine out of 10 banks report that Open Banking has made their operations more efficient. However, 56% of institutions see regulatory uncertainty as a significant barrier. Closer cooperation between regulators and the fintech industry is essential to develop a clear policy framework that supports sustained innovation.

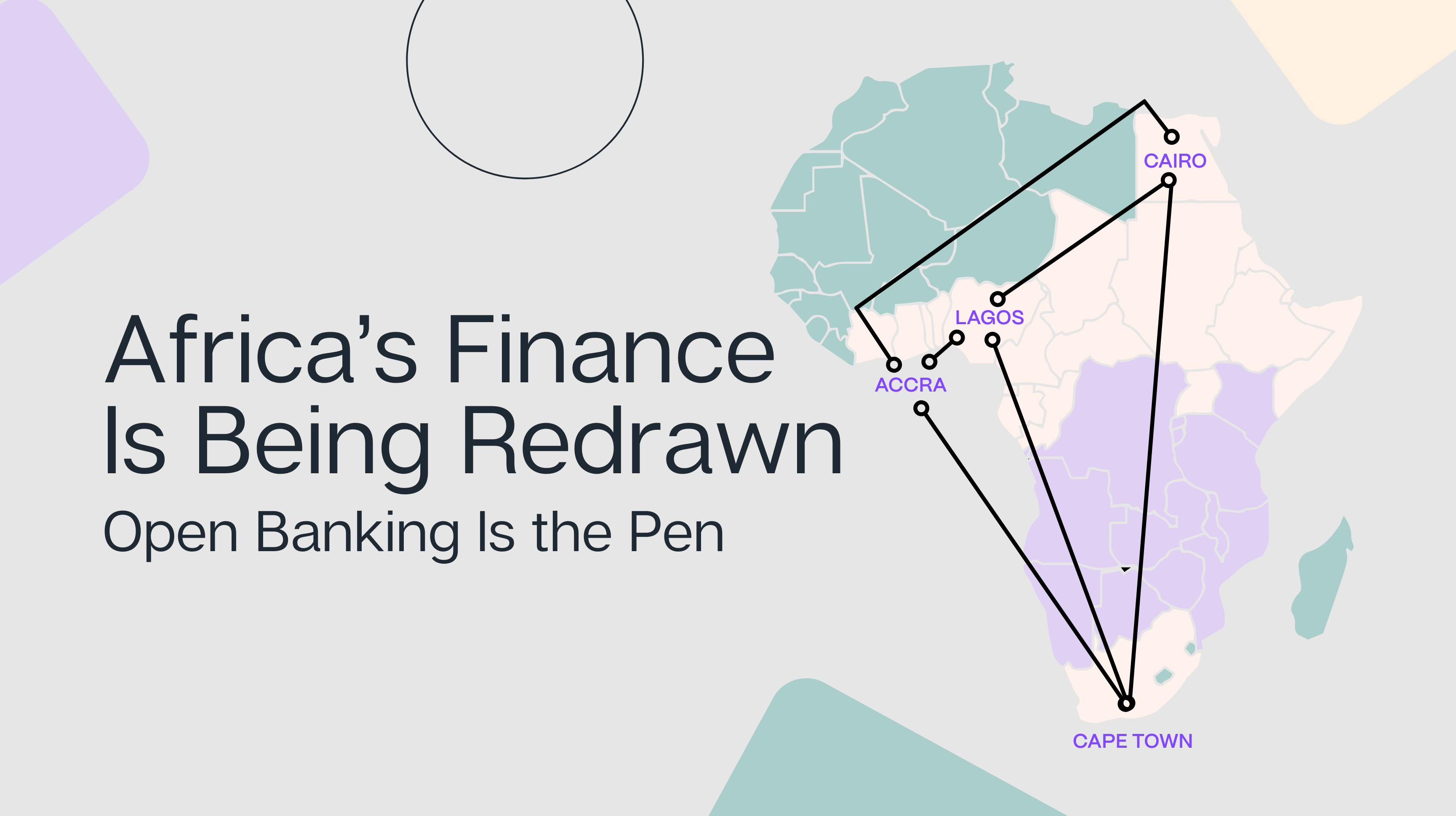

- India: The second most populous country in the world is pioneering Open Banking with initiatives like ONDC and India Stack. The first one builds an open e-commerce network that integrates banks to simplify payments across the country. India Stack uses Aadhaar (a national digital ID system that verifies identity across services) and UPI (Unified Payments Interface – a real-time network for instant bank transfers) to extend banking to isolated, remote areas.

- Japan: Open Banking in the country of the rising sun is unfolding through a softer, non-mandatory approach. Instead of strict regulation, innovation is being driven by forward-thinking banks and fintechs exploring APIs and testing digital collaborations. Since Japan introduced its legal Open Banking framework in 2017, major players like MUFG and SBI have taken the lead by enabling secure data sharing with fintech partners—paving the way for a more connected, user-centric financial ecosystem.

- South Korea: It’s no surprise that this tech-savvy nation is leading the way in Open Banking across Asia. Thanks to a progressive blend of regulatory support and market-driven innovation, digital-first banks like KakaoBank and K Bank are at the forefront. These institutions offer mobile-only services that have redefined banking convenience and accessibility. KakaoBank alone attracted 240,000 users on its launch day and surpassed 14 million by 2021. With a fully digital model and no physical branches, South Korea proves how innovation and user-centric design can reshape finance.

- China: The most populous country in the world is redefining open banking through massive digital ecosystems rather than traditional Western-style models. Powered by giants like Alibaba’s MyBank, Tencent’s WeBank, and Xiaomi-backed XWBank, these digital-only banks leverage vast consumer and transaction data from platforms such as Alipay and WeChat Pay to offer fast, automated financial services. State-owned banks, once slow to innovate, are now adopting API-driven open banking to stay competitive amid economic and regulatory changes. China’s platform-based finance model bypasses traditional frameworks, boosting financial efficiency.

Key Takeaway for Businesses:

Asia’s fast-paced adoption of open banking sends a powerful message to merchants: thriving in new markets means forging smart digital partnerships and harnessing the power of data-driven innovation. To seize these opportunities, companies have to stay agile and stick to ever-changing regulations—turning challenges into opportunities.

The 3 Winning Models Moving Forward Asia’s Financial Future

As Open Banking evolves across Asia, three main business models have emerged for digital banks: the orchestrator, the distributor, and the aggregator.

1. Orchestrator: The Collaborative Approach

This model serves as a dynamic marketplace where banks join forces with partners like digital lenders and payroll providers to launch innovative products together. Built on strong partnerships, the orchestrator enables real-time, secure sharing of regulated banking services via open APIs. This collaborative ecosystem enhances customer satisfaction by refining offerings based on direct feedback.

2. Distributor: Fintech as the Frontline

Financial institutions collaborate with fintech firms, acting as distribution channels. While the banks concentrate on customer acquisition and managing product responsibilities, fintech partners handle servicing. This setup enables rapid customer base expansion while maintaining control over core operations such as account management.

3. Aggregator: Connecting the Data Dots

It centers on gathering diverse digital services and data—from KYC and onboarding technologies to insights on customer spending, saving, and borrowing behavior. Banks leverage this aggregated data, often through multiple third-party collaborations, to deliver a seamless, transparent, and personalized user experience. This enhances customer satisfaction by offering tailored financial solutions.

Key Takeaways for Businesses:

To thrive in Asia’s evolving Open Banking landscape, businesses have to adopt collaboration, leverage fintech partnerships, and harness data-driven insights. Whether orchestrating ecosystems, distributing products through agile fintech channels, or aggregating data for personalized experiences, success hinges on agility, secure API integration, and customer-centric innovation. Aligning with these models ensures new growth opportunities.

Asia Rewrote The New Rulebook—In Real Time

The East has redrawn the rules of engagement. Banks in Asia are no longer going it alone—they’re co-creating with fintechs to deliver what matters most to clients: frictionless, data-driven experiences.

The shift demands new thinking: orchestrate collaborations, distribute through nimble channels, and aggregate for insight. In this frontier, loyalty is not given—it’s earned through value, built on trustworthy partnerships.

Just like Asia’s leading fintechs, Contiant engineers loyalty through agility. We simplify the complexities of today’s financial landscape, enabling businesses to stay ahead with seamless API integration and cloud-native solutions. The platform empowers companies to navigate regulatory shifts effortlessly, leverage emerging fintech opportunities, and scale with confidence. By strengthening agile partnerships and providing reliable, future-proof infrastructure, Contiant turns complex challenges into powerful growth opportunities. This enables businesses to stay competitive and thrive in an ever-evolving global marketplace.

Stay tuned for Part 2 of ‘Travel the Globe with Contiant,’ where we’ll explore the rising Open Banking landscapes of Latin America!

.png)

.jpg)

.png)

.png)