Contact us

Our friendly team will love to hear from you!

How Open Banking is Transforming Finance in Africa

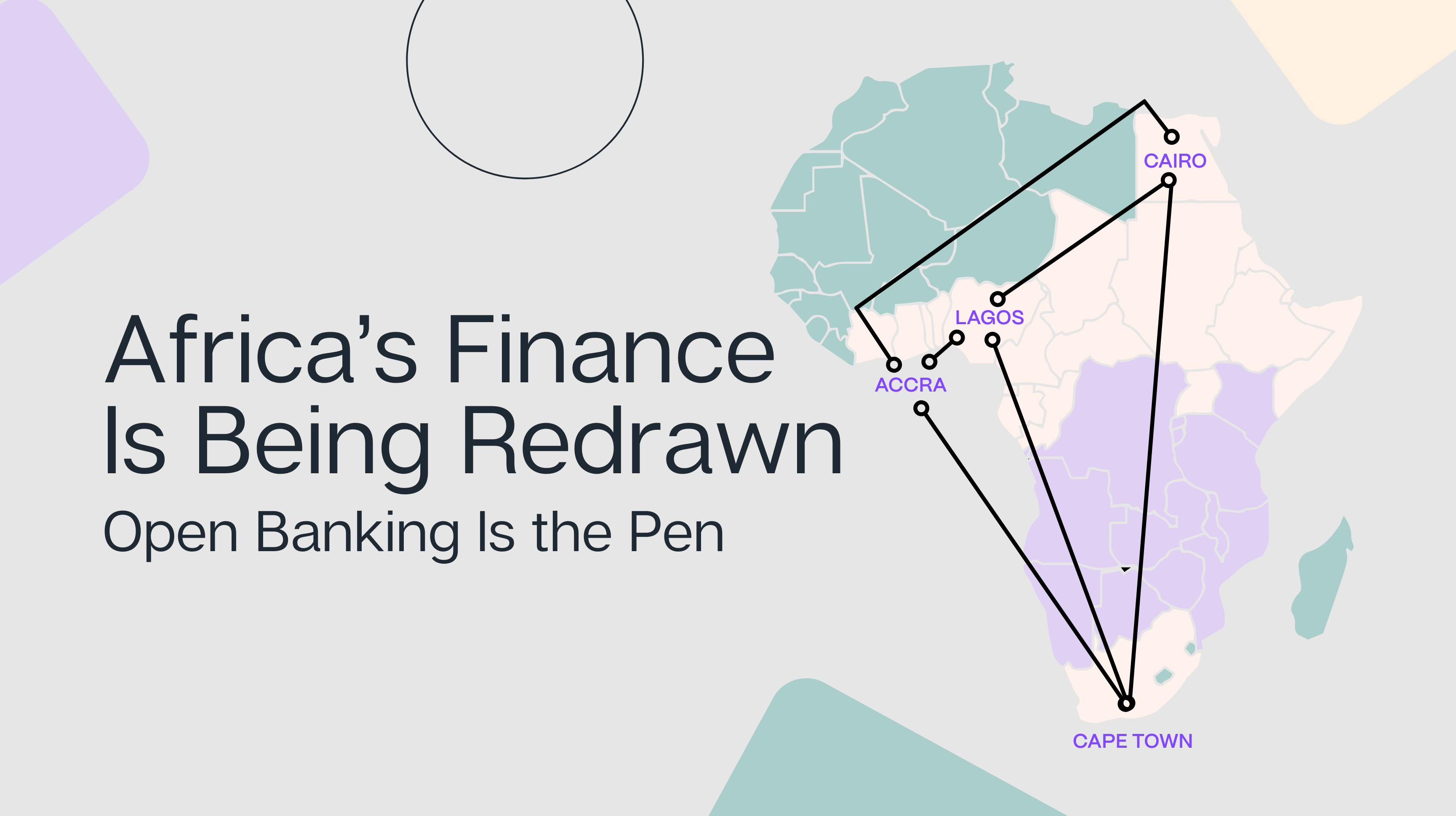

Redrawing Africa’s Financial Map with Open Banking

The Continent’s financial story isn’t unfolding in a straight line. It’s a vibrant script of mobile wallets, cash-driven markets, ambitious fintechs, and regulators racing to catch up. From Lagos to Cairo to Cape Town, new digital rails are being built not only to move money faster but to redefine access, cost, and trust in finance. Instead of repairing cracks in the old system, Africa is laying down fresh blueprints for finance.

This article explores how Open Banking is driving that transformation across Africa, reshaping payments and laying the groundwork for growth.

The Wind of Change Now Blows as a Storm of Transformation

Three powerful currents are colliding across the continent. Regulation is clearing the skies around data-sharing. Instant payments are rushing in to sweep away friction and cost. Banks, fintechs, and telcos are converging like a weather front. What began as a breeze of change has grown into a storm of transformation that is reshaping how people pay, borrow, and onboard into financial services.

Africa’s Big Four in Focus

Nigeria Pushes the Start Button

The country didn’t wait around. In 2021, the Central Bank laid down the Open Banking rulebook, and by 2023, it had filled in the details on who can participate, how consent works, and what data is shared. With the rules clear, the real action is about to begin: subscription payments that actually work, payroll-linked loans that make credit fairer, and smarter collections for small businesses.

For lenders, this enables more accurate checks on affordability.

For businesses, it brings cash flow they can rely on.

Ghana’s Challenge: Banking Growth in a Cash-First Market

Heading west, where almost everyone has a phone, but most still pay in cash. Last year, fewer than 40% of adults had a bank account, and over 60% of transactions stayed cash-based. That leaves too little banking data to judge creditworthiness or streamline onboarding. The answer lies in blending: banks bring what they have, telcos add the missing pieces like identity and income signals. Once regulators clear the way, this approach could bring fair credit to far more people.

Egypt Connects the Nation in Real Time

The land of timeless wonders flipped the switch on its Instant Payment Network (IPN) in 2022, giving consumers 24/7 real-time transfers through InstaPay. This national rail makes payments cheaper than cards, speeds up settlement, and sets the stage for account-to-account checkout and request to pay.

As adoption grows, merchants save money and fintechs build new services on rails as steady as the Nile.

South Africa Lifts the Curtain on Finance’s Next Act

The country’s finance scene used to move through backroom deals between a few big banks. Not anymore. In March 2024, the Financial Sector Conduct Authority laid out plans for a phased, mandatory Open Finance model. The vision goes beyond payments to include wider financial products and true data rights for consumers.

Coming next: clearer rules and standards that protect consumers while opening new opportunities for innovation.

The Bottom Line for Businesses: Why Now Is the Time to Move

What used to be slow, manual, and cash-heavy in Africa is giving way to faster, smarter, and safer systems. From Lagos to Accra to Cape Town, fresh rules and digital rails are changing how money moves, how credit is given, and how trust is built across the sunny continent.

1. Payments: Instant rails combined with shared data with user permission are making pay-by-bank not only possible but affordable. The result is smoother checkout, smarter recurring payments, and easier collections, a big win for subscriptions, utilities, gaming, and digital commerce. In markets like Nigeria and Egypt, early trials are turning into everyday reality as rules and infrastructure improve.

2. Credit & risk: In places like Ghana, where bank data is limited, lenders can fill the gap by adding other sources such as telco records, payroll data, or merchant platforms. This mix helps them offer loans to thin-file customers while still keeping risk under control. The aim is to build a fuller, more reliable picture of customers rather than take on unnecessary risk.

3. Compliance & onboarding: Standardized APIs take the hassle out of paperwork. They cut down on manual KYC checks, make consent something that can be managed continuously, and give regulators the clear audit trails they need. This is becoming even more important as countries move from optional data sharing to strict rules with strong safeguards and advanced security.

The shift is clear: faster payments, fairer credit, and safer onboarding are no longer distant goals but active priorities. For businesses, the opportunity is to ride these changes instead of resisting them. The winning move is to adapt early rather than scramble later.

Contiant Connects the Dots in Open Banking

Connecting the dots in Open Banking starts with strong foundations: secure data links, instant payment flows, and compliance tools built for local rules. With these in place, Contiant helps businesses move faster, stay compliant, and scale with confidence.

The platform:

- Brings data together: Combines bank, telco, and payroll information into one secure stream to check income, verify affordability, and better understand customers.

- Simplifies payments: Powers pay-by-bank, request-to-pay, and recurring payments while handling the local rails and settlement behind the scenes.

- Bakes in compliance: Captures consent, keeps detailed audit trails, and adapts to new rules in Nigeria, Egypt, South Africa, and beyond.

The outcome: faster onboarding, higher approval rates, lower fraud and fewer chargebacks, and significantly lower payment acceptance costs so you can scale in Africa’s fastest-growing markets with confidence.

The Strategy Checklist: Put It to Work Today

✔ Map priority markets by regulatory readiness (for example, Nigeria’s guidelines and South Africa’s pending mandate).

✔ Identify the real-time rails you’ll use (such as Egypt’s IPN) and design A2A checkout and collections.

✔ Expand your consented data strategy beyond bank data in thin-file segments by pairing with telco or payroll data.

✔ Set up VRP, subscriptions, and recurring collections to ensure predictable cash flow.

✔ Work with partners that deliver standards-based security and auditable consent. Choose Contiant.

Africa isn’t copying models from elsewhere; it’s building its own. With smart orchestration of data, payments, and compliance, Open Banking turns access into unstoppable growth.

This article is one stop on our Open Banking Global Tour, where we explore how different markets build their unique paths to finance.

.png)

.jpg)

.png)

.png)